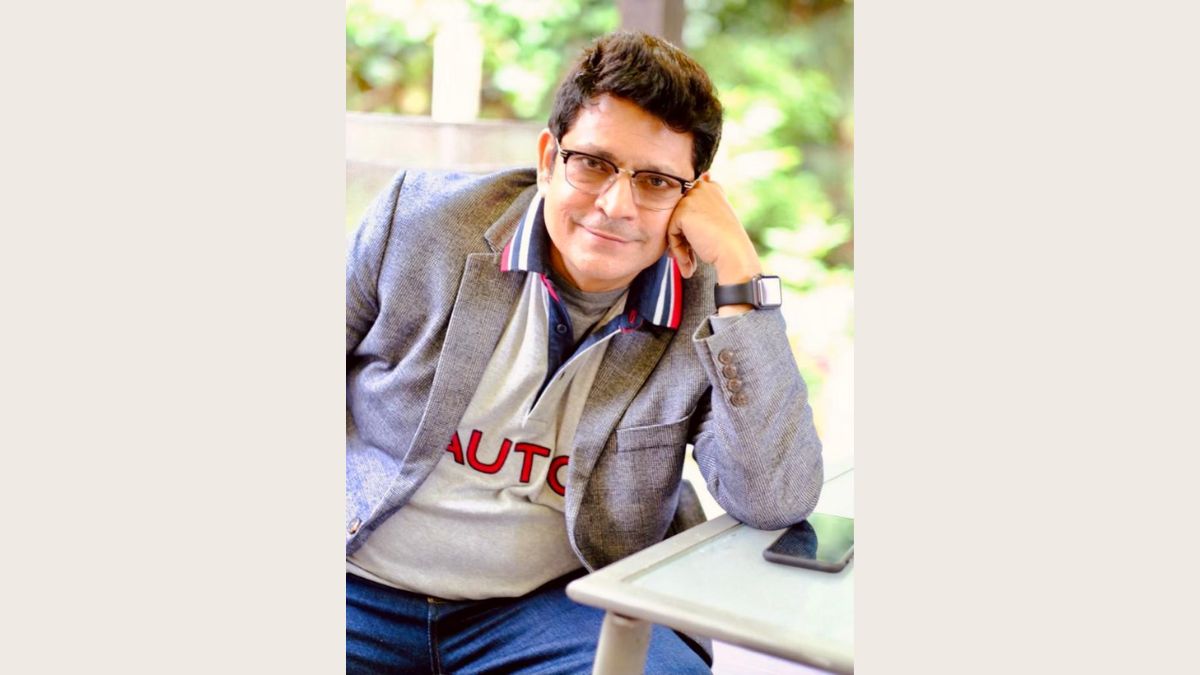

S Anand, the Chief Executive Officer and Co-Founder of PaySprint

How will you introduce yourself to the world?

I am S. Anand, I am a Techno functional professional with over 2 decades with diverse career chronicle working with cross-functional teams to drive unprecedented profitability while focusing on operational excellence, streamlining business processes and cost

I have extensive leadership and management experience in setting up operations and running a business in high growth as well as transformational phases. I have built teams with capabilities to drive results in a fast-paced and continually changing environment. Ability to see the ‘big picture’ - understand and simplify complex situations & business challenges, design and deliver success for all stakeholders by implementing innovative business solutions.

Being an integral part of the Top Management, have a complete understanding of critical business drivers and the skills to use business intelligence for creating a meaningful interaction with clients and delivering on time, as per budgets while achieving top and bottom line targets. A decisive, straightforward and energetic executive who leads by example, consistently galvanizes his teams to action, and is laser-focused on results. Technical Know-how, stellar communication skills, and ability to advance new initiatives are key differentiators.

A motivational leader with core strengths around technical leadership, leading large diverse teams, thought leadership & experience in putting together strategy for contingency plans & process automation(s). An enterprising People leader with sensitivity to the dynamics of cross-cultural workspaces, leading a large group of multinational teams ensuring the “Employee Experience” at the workplace is at its best

Tell our readers about your achievements till today

- Pivotal in making Eko emerge as the No.1 player in the Remittance / AePS / Bill payment / Recharges in India by using various Process Re-engineering initiatives, thereby maximizing its short, medium & long-term profitability and shareholder returns

- Played a key role in driving Eko / Sterlite / Tata Tele SME into an EBITDA +ve company and augmented penetration from 30% to 200%

- Conferred with Job Awards & Leadership Award across functions for Leadership Qualities as a recognition for showcasing outstanding leadership attributes

Notable Accomplishments

- Acknowledged as Best Post-Paid Sales Manager, awarding 1 Mn Celebration in Idea from MD of Idea Sanjeev Agha

- Winner of the Chairman’s Trophy for the Best Clustering B2C Sales which included Pre-paid, Post-paid & Retail Sales across India from Mukesh Ambani

- Conferred with:

- Best Innovative Money Transfer Product Award at IAMAI India Digital Summit in 2018 & 2020

- Graham Bell Awards 2015 for creating a Connected Community in Hiranandani Chennai for Sterlite

Tell us about your start-up!

PaySprint is a Fintech venture focussed on NextGen Neo Banking Solutions, offering a Unified Open API Platform.

The Year 2020 saw India and Bharat coming to age on digital payments both on payments and acceptance. This has been purely been possible through JAM - JanDhan Accounts, Aadhar & Mobile / smartphone penetration. Keeping the above 3 as core and the need for better, faster & easier technological solutions, we have launched PaySprint in 2020. Our mission is to enable and enhance financial inclusion and literacy among audiences by offering holistic solutions for complete financial support. At PaySprint, we are pioneering strong partnerships with the Banking ecosystem and provide Unified Open API Platform that would transform how Bharat transacts and leads to larger consumer adoption, interface and delight.”

The PaySprint API’s are powered to cater to the requirements of multiple enterprises, across multiple geographies. PaySprint’s interactive dashboard leverages API-first architecture allowing third-parties to connect easily to create an open banking ecosystem to ensure businesses have access to the best business products and practices

"What's the most important thing you're working on right now, and how are you making it happen?

Right now the focus is on UPI and various products / services based on UPI.

About UPI

The Unified Payment Interface (UPI) provides a single interface that allows seamless interoperability between different payment systems.

How it works

- UPI works on the concept of a virtual payment address.

- Bank accounts, cards and wallets can be mapped to a unique virtual payment address.

- Payments can be made using an account number, mobile number and Aadhaar number (virtual payment address).

- UPI leverages the existing infrastructure for authentication.

UPI’s benefits, Success & Growth

- The use of a virtual payment address affords interoperability and makes one-click payment possible.

- Funds transfer can be initiated by either the payee or the payer.

- UPI eliminates the need for exchanging sensitive information, such as bank account numbers, one- time passwords or phone numbers during a financial transaction.

- 2200 million transaction in Dec’2020 & 200 million plus active monthly users

- CAGR of 414% since inception in 2016 & 40% P2M out of total UPI transactions

- Projected UPI transactions growth is likely to be 7X by 2025.

We are working closely with Banks / NPCI to create unique solutions around UPI. We will be announcing the launch soon.

What's your take on your segmented/targeted Market?

Our Focus to B2B, B2B2C.

PaySprint offers developers the ability to build a vast number of use cases leveraging our API’s and target customers are Entrepreneur’s, Startup companies, Banking partners, NBFCs, MSME’s & Enterprises who can either use or deploy these solutions

What are the challenges you have faced and what are the current challenges? Mention the top three challenges for both

Top Three Challenges

- Faster rollout of API’s impacted by Covid

- Faster conversion impacted by Covid

- Awaiting Seed Funding

Why have you started up?

A decade ago, RBI introduced NEFT and RTGS, followed by NPCI introducing IMPS, and this was a start of digital or online banking and a paradigm shift in the way services were offered to the end consumer. The next stage of evolution was from internet banking to API led Banking.

The dawn of API in banking has resulted in significant changes concerning how financial operations are carried out.

Although APIs have been widely used for over a decade, their use has recently become prevalent in financial services

Benefits of API banking and how is it causing a Revolution?

- With API banking, innovators have more flexibility to provide the best features and services to streamline financial services.

- Have reduced many administrative hurdles with regard to managing customers own finances like applying for a business loan, checking your creditworthiness, and many more

- Have a single view of customers all finances while being able to control, track, and analyse all financial movements, all in one place

- API banking has led to lowering the costs in a way that it is now more economical to serve the underserved and unbanked and offer products and services better suited to their needs.

- Today Fintech’s are using API Banking to retrieve account balances in real time, processing transactions at high speed round the clock,

- API Banking provide enhanced information for reconciliation in real time, process vendor and dealer finance transactions real time thereby facilitating faster churn in the ecosystem

The most important fallout of API Banking is the data analytics which lies at the heart of the banking API revolution. Banks can now collect substantial quantities of data relating to customer behaviour, which should, in turn, enable them to create more tailored product & services and also specific marketing initiatives.

Today Banks are convinced that in order to grow and extend the Banking solutions beyond their own banking Channels and technology and in order to achieve larger adoption of their financial services they need strong partnership with Fintech’s thru API Banking, so thereby API Banking is truly creating a Revolution in Banking.

PaySprint having understood the importance of API Banking and in order to solve the problem of not having innovative solutions for Digital Banking that can create larger customer delight and interface, and which can lead to larger adoption have taken this initiative to start this new Startup PaySprint

Where do you want to see yourself in the next 5 years?

Our ambition is to become a Unicorn.

Please share your learning for fellow Entrepreneurs?

- Be Passionate about your Idea

- An Idea should solve a Problem

- Think innovative and Act fast

- Create an inspired team

- Dare to Dream, Dare to fail & Dare to Succeed

Do you see the current regulations of country offer a level playing field to fintech players

We are at a time where the Government, RBI, NPCI, Banks and the entire ecosystem are very supportive to the fintech players and have also created regulations which support innovation along with compliances

What you see as top three entry barriers in the segment

- Understanding of Technology

- Understanding of Tax Regime especially the GST

- Understanding of Banking Solutions and the unique use cases it can solve.

If you are given a chance to suggest a policy change, what would that be?

One Policy Change would be as below

- UPI which works on the concept of a virtual payment address.

- Currently Bank accounts, Debit cards and wallets can be mapped to a unique virtual payment address.

- A policy change to allow Credit Cards to be mapped to the unique virtual payment address

- Which means Credit card Payments can be done by using the QR code for small transactions only.

The MDR charges like now can be borne by the merchant